The U.S.–China technology landscape is more nuanced than the headlines suggest. For investors, operators, and policymakers, the path to sustained leadership runs through ecosystems, and the window for building them is narrowing.

The conventional framing of U.S.–China tech competition tends toward extremes. China is either portrayed as unstoppable, given its dominance in electric vehicles, batteries, and solar panels, or dismissed as lacking the creative capacity to push the technological frontier. The United States is either celebrated as the unquestioned AI leader or criticized for losing its manufacturing base and becoming dangerously dependent on rivals.

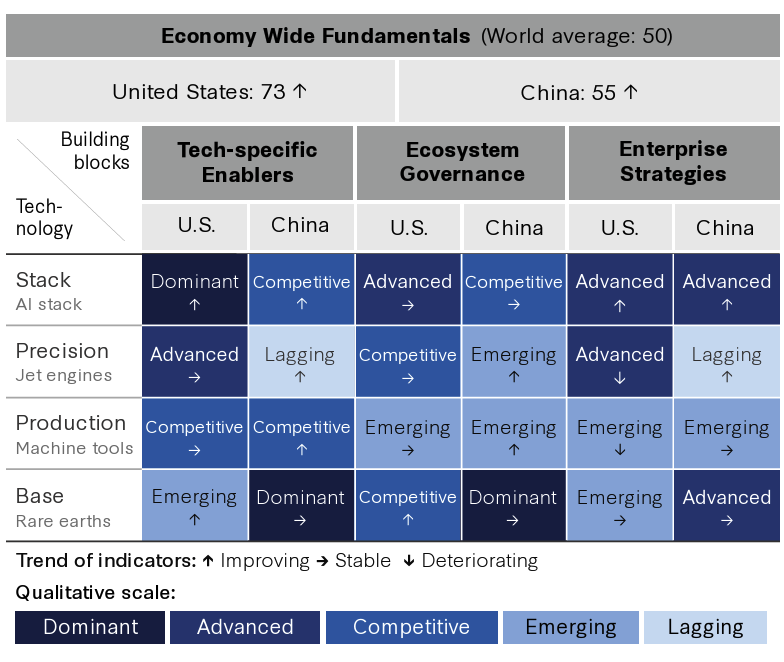

The reality, as a recent CSIS analysis lays out in detail, is far more instructive. In 2025, China made meaningful AI progress under chip constraints, achieved breakthroughs in robotics and quantum computing, and weaponized its control of rare earth processing. Yet China still cannot produce a certified jet engine or compete in high-end machine tools. The United States controls 90 percent of AI chip markets and produces far more advanced AI models than China, yet it has lost much of the manufacturing capacity needed to build at scale and depends on rivals for critical materials.

These patterns cannot be explained by looking at R&D budgets or patent counts alone. The more useful lens is technological dexterity: the ability to build strengths across different technology types, where advantages in one domain compound advantages in others. AI chips enable AI models. Rare earth processing enables chip manufacturing. Machine tools enable precision aerospace components. These technologies reinforce each other, but only when the right ecosystems support them.

At Nestpoint, where our positions span energy, robotics and AI, capital markets, and technology sovereignty through our Sovereign Shield initiative, this ecosystem-level view of competitiveness has shaped our approach from the start. Technology leadership is not won by individual breakthroughs alone. It is won by the dynamic combinations of firms, researchers, institutions, policies, and allied networks that turn lab discoveries into factory output and individual capabilities into networked advantages deployed at speed and scale.

Four Technology Types, Four Different Playbooks

Understanding where the U.S. leads and where it lags requires looking at technology through four distinct categories, each defined by breadth of application and production complexity. Each demands a different combination of ecosystem building blocks, and achieving dexterity across all four is the strategic imperative for the United States.

Stack Technologies (e.g., AI and advanced chips) require deep capital markets, collaborative research networks, and platform orchestration. The United States leads here, controlling 90 percent of AI accelerator markets and producing 40 notable models compared to China's 15. This is the domain where American venture capital, research universities, and open innovation culture create compounding advantages.

Precision Technologies (e.g., jet engines and lithography) demand decades-long partnerships and rigorous certification regimes. The United States and its allies lead here as well. Despite sustained prioritization by Beijing, China still has no certified commercial jet engine in flight. These moats are formidable and reflect institutional depth that cannot be replicated quickly.

Production Technologies (e.g., high-end machine tools) need patient capital and continuous vocational training. Here the picture grows more complicated. The United States has lost historical advantages, and China also remains unable to enter high-end tiers. The European Union and Japan lead through dense supplier networks and continuous vocational talent cultivation.

Base Technologies (e.g., rare earth elements, batteries, steel, and aluminum) require coordinated supply chains and processing infrastructure. China dominates this category, processing 90 percent of rare earths and producing more steel than the rest of the world combined. This dominance was built through decades of mercantile policy, including below-cost dumping that has eroded Western capacity.

The interdependencies across these categories are what matter most. Base technologies enable Stack technologies: without secure critical mineral inputs, chip design advantages become vulnerable to supply disruption. Production technologies determine scaling capacity: without machine tools, America cannot scale Stack or Precision technologies at home. China now threatens to do to Stack technologies what it has already done to Base technologies, capturing commercialization and diffusion while America retains invention but struggles with deployment.

The Ecosystem Gap: Where America Excels and Where It Falters

Four building blocks underpin ecosystem strength across all technology types:

- Economy-wide fundamentals such as macro stability, rule of law, and factor markets

- Technology-specific enablers such as R&D infrastructure, IP rights, standards, and workforce and talent pipelines

- Ecosystem governance such as public-private coordination and adaptive regulation

- Enterprise strategies such as innovation cycles, production networks, and intra-firm linkages

Across technology types, the United States excels at frontier research but struggles with the capital-intensive engineering, testing, and scaling phase between lab and market. This "missing middle" is where learning curves are ceded to competitors. America invents, but diffusion lags, limiting the payoff from its Stack leadership.

America's advantages rest on foundations that China struggles to match: open collaboration, institutional trust, global talent attraction, and the capacity to orchestrate complex partnerships with allies. But vulnerabilities compound when these strengths are not paired with the patient capital and industrial infrastructure needed to move from invention to production at scale.

Meanwhile, China deploys a set of mercantile and malign tools that have systematically eroded Western capacity: below-cost dumping that bankrupts competitors, forced technology transfer, coercive licensing, predatory investment, and patient state capital that can tolerate prolonged periods of losses to capture entire supply chains. Export controls and tariffs address symptoms but cannot substitute for building domestic and allied capacity.

Why Private Capital Must Step Into the Gap

Government action alone will not close the ecosystem gap. Patient capital, applied with strategic intent, is essential for rebuilding capacity in energy infrastructure, advanced manufacturing, and the data systems that underpin robotics and AI deployment.

This is the bind: America relies primarily on historical strengths, including capital markets, universities, and the rule of law, without adequate tools to counter China's practices at the ecosystem level. Breaking the bind requires building new capabilities, including patient capital mechanisms where strategic necessity demands them, conduct-based trade tools that counter dumping and coercion without broad protectionism, allied coordination that pools resources and shares burdens, and institutional capacity to execute multiyear strategies across political transitions.

Private equity firms with deep sector knowledge are uniquely positioned to fill this role, particularly in Base and Production technologies where the gap between policy ambition and deployed capability is widest. Strategic investors who understand both the technology and the regulatory landscape can move faster than government programs and more patiently than venture capital, funding the "missing middle" that determines whether American inventions become American industries.

Energy as the Foundation: Securing the Base

Of all the technology gaps facing the United States, the erosion of Base technology capacity carries the most structural risk. China's dominance in rare earth processing, battery manufacturing, and steel production was the product of decades of systematic investment, state-backed capital, and mercantilist trade practices that bankrupted Western competitors. The toolkit behind that dominance is well documented: below-cost dumping, forced technology transfer, coercive licensing, predatory investment, and patient state capital that can absorb years of losses to lock down entire supply chains.

Rebuilding Western capacity in energy and critical materials is foundational to every other technology priority. Without secure energy inputs, advances in AI chips, robotics, and precision manufacturing remain vulnerable to supply chain disruption. The Defense Production Act should be deployed for Base technologies like critical minerals where patient capital requires government de-risking, and the private sector must be ready to meet that moment with operational capacity and domain expertise.

This conviction shapes Nestpoint's energy investments. Our portfolio company DHC Power operates at the intersection of energy infrastructure and the critical systems that support technology sovereignty. Companies like DHC Power represent the kind of energy infrastructure investment that turns policy ambition into deployed capability, building the Base layer that every other technology category depends on.

Robotics, AI, and the Data Layer That Connects Them

Robotics sits at the intersection of all four technology types, making it one of the clearest tests of ecosystem dexterity. Robotic systems depend on AI (Stack), precision components (Precision), machine tools (Production), and critical materials (Base). China achieved notable breakthroughs in robotics in 2025, and the broader competitive landscape makes clear that achieving dexterity in this domain requires strength across the full technology spectrum.

What is increasingly clear to practitioners in the field, even if underexplored in most policy analyses, is the critical role of spatiotemporal data infrastructure in enabling robotics at scale. Autonomous systems, whether operating in logistics, defense, agriculture, or infrastructure inspection, require high-fidelity spatial and temporal data to perceive, navigate, and act in the physical world. As robotics moves from controlled environments into complex, real-world operating domains, the quality and accessibility of spatial data becomes a rate-limiting factor.

Spatious Data, a Nestpoint portfolio company focused on spatiotemporal data for robotics, is building the data layer that addresses this gap. Their work sits squarely within the technology-specific enabler category: the infrastructure that determines whether inventions translate into deployed, scalable capabilities. Without this data foundation, even the most advanced robotic systems remain confined to narrow use cases.

Technology Sovereignty and the Allied Dimension

Allied coordination is perhaps the most consequential and underappreciated dimension of the technology dexterity challenge. The United States should lead and institutionalize a new multilateral regime focused on a broader definition of dual-use technologies, negotiate tech-friendly trade compacts, and create mechanisms for sharing costs and deepening coordination with allied nations.

As governments worldwide prioritize technology sovereignty, demand is accelerating for partners who can navigate the complexities of regulatory compliance, security clearances, and cross-border technology transfer. Nestpoint's Sovereign Shield initiative was designed to meet exactly this need. We invest in companies uniquely positioned to serve the growing market for allied technology domestication, combining deep federal contracting experience with the agility to support allied domestication programs.

One of the more compelling policy proposals gaining traction is a Technology Dexterity Fund that would pool funding from the Departments of Defense and Commerce, alongside private American investors and allied and partner capital, to invest jointly in U.S. technology capabilities. This kind of coordinated public-private-allied investment framework aligns closely with the Sovereign Shield thesis: that the next generation of technology leadership will be built through trusted partnerships that adversaries cannot penetrate.

Three Reinforcing Strategies for the Road Ahead

Achieving technology dexterity demands three self-reinforcing strategies, each carrying direct implications for how capital should be deployed:

Playing All the Keys. America must secure Base inputs, strengthen Production capacity through selective reshoring and allied networks, fortify Precision technology moats without sheltering incumbents, and compound Stack advantages through faster scaling and diffusion. CHIPS Act science funding should be focused on Base and Production technology gaps, directing billions in research authorization toward time-bound commercialization grand challenges, especially where Chinese mercantilism has eroded Western capacity.

Achieving Speed and Scale. Permitting shot-clocks with enforcement teeth should rapidly cut timelines for mining and infrastructure projects from decades to years, and from years to months. Commercialization bottlenecks, where innovations die between lab and factory, must be broken. Manufacturing USA and similar programs should be refocused on end-to-end pilot lines to rebuild shared engineering infrastructure and test datasets. Federal and state governments should launch sector-specific adoption accelerators and prioritize workforce development with portable credentials in desperately needed skilled trades such as electricians and technicians.

Defending the Network. Safeguarding innovators, networks, and their innovations requires dedicated "fast-action" teams specialized in high-clockspeed industries and adversary reactions. The government should impose conduct-based import restrictions on below-cost dumping, coercive licensing, and predatory investment rather than blanket sectoral bans. CFIUS authorities should be expanded, and a central economic security capability should be created for coordinating across government.

The Window Is Open, but Narrowing

If 2025 delivered wake-up calls, 2026 demands action. Congress and the executive branch will either unify around technology leadership or fracture into tariff wars and political skirmishes that squander the very advantages China cannot replicate.

Public funding under CHIPS and Science Act authorities, refocused today, can enable targeted breakthroughs tomorrow. Inaction will see nascent U.S. technologies fail to scale because of the "missing middle." Early moves toward a Technology Dexterity Fund could build confidence among allies and supply chain partners. Permitting and regulatory reforms at the federal and state level, enacted now, can turn infrastructure potential into deployed capacity. Without those reforms, projects envisioned today could languish until after 2050.

The United States has rebuilt ecosystem advantages before. DARPA's creation of the internet, the biotech revolution sparked by the Bayh-Dole Act, and rural electrification succeeded because the government, private sector, universities, and workers aligned around shared objectives. Americans are losing time, and the question is whether the country will reassert its scientific, engineering, and manufacturing prowess, especially where it has lost ground, or whether it will continue to cede leadership.

At Nestpoint Group, we believe the answer lies in strategic capital deployment across the technology domains that matter most: energy infrastructure that secures the Base, spatiotemporal data and AI systems that power the next generation of robotics, capital markets innovation that funds the transition, and Sovereign Shield partnerships that ensure allied nations can build and sustain their own technology sovereignty. The analytical frameworks are available. The work of building these ecosystems, company by company, is where the real advantage is forged.

This post draws on findings from the CSIS Center for Strategic and International Studies' Tech Edge: A Living Playbook for America's Technology Long Game (2025).