Robotic Manufacturing Inflection Point

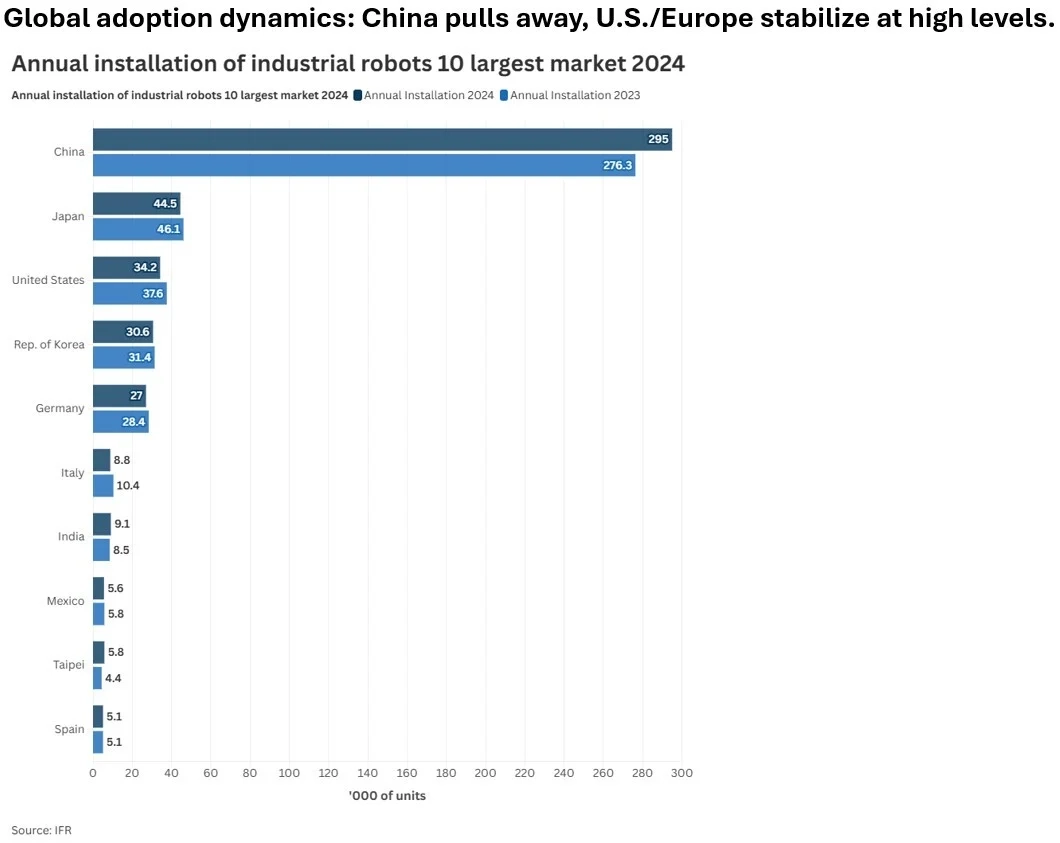

The global robotics industry crossed a threshold in 2024 that deserves more attention than it received. For the first time, Chinese domestic robot manufacturers outsold foreign suppliers on their own soil, capturing 57% of the Chinese market, up from 28% a decade ago. China installed 295,000 industrial robots that year, more than the US, Japan, Germany, and South Korea combined. Its operational robot stock now exceeds two million units, the largest of any country on earth.

These are not projections. They are deployed machines on factory floors, and they represent a structural shift with enormous implications for economic competitiveness, national security, and capital markets.

The Installation Gap

Global robot installations hit 542,000 units in 2024, the second-highest annual count on record, according to the International Federation of Robotics. The global operational stock reached 4.66 million units, up 9% year-over-year.

Asia accounted for 74% of new installations, Europe 16%, and the Americas just 9%.

The IFR projects installations will reach 575,000 in 2025 and surpass 700,000 by 2028. In the first half of 2025 alone, China's industrial robot production surged 35.6%, reaching nearly 370,000 units in six months.

China's robot density, 470 units per 10,000 manufacturing employees, now exceeds both Germany and Japan. This reflects deliberate national strategy: China's RMB 1 trillion (~$138 billion) VC Guidance Fund, Shanghai-specific robotics subsidies, and targeted incentives under the 14th and 15th Five-Year Plans have turned deployment into an infrastructure priority.

The United States installed 34,200 units in 2024, outpaced roughly nine to one.

Capital Is Moving

Private markets have noticed. Robotics deal values hit a record $107 billion in 2025, growing at a 10-year CAGR of 22% per FactSet. But capital flows differently by region. US deals skew massive, some exceeding $50 billion, reflecting the depth of American venture ecosystems. European and Chinese deals average under $10 billion, concentrated in precision engineering and supply chain optimization, respectively.

Several transactions illustrate the intensity of the cycle.

- SoftBank agreed to acquire ABB's robotics division for $5.375 billion in October 2025, explicitly to build a "Physical AI" platform by combining ABB's installed base with its AI-adjacent portfolio.

- Figure AI, the US-based humanoid company, closed a Series C north of $1 billion at a $39 billion valuation, backed by NVIDIA, Intel, and Microsoft.

- Neura Robotics in Germany raised $1.2 billion in March 2026, reaching a $4.6 billion valuation through partnerships with Bosch, Hyundai, and Qualcomm.

- Amazon made perhaps the most telling move of 2026, acquiring two robotics companies in a single week: Swiss delivery firm Rivr and New York-based Fauna Robotics, maker of the Sprout consumer humanoid.

Big Tech now treats robotics not as a research project but as a core business line, one where consumer humanoid acceptance remains a critical variable, and where US companies are racing to close the gap on a market China currently dominates with 85% of humanoid deployments.

Tesla's Bet: Cars to Robots

No company captures the pivot more dramatically than Tesla.

In January 2026, Musk announced that Tesla would end Model S and Model X production and convert those Fremont factory lines to produce Optimus humanoid robots at a target rate of one million units per year. Tesla simultaneously broke ground on a dedicated Optimus facility at Gigafactory Texas with ambitions of ten million units annually.

This is a remarkable capital allocation decision, voluntarily walking away from proven automotive revenue for a product line that has yet to generate meaningful sales. But the logic is clear: if humanoid robots can perform general-purpose labor at scale, the addressable market dwarfs passenger vehicles.

The global humanoid robot market is projected to grow from roughly $6 billion in 2026 to $165 billion by 2034, a 50.6% CAGR.

Tesla has already deployed over 1,000 Optimus Gen 3 units across its own factories for autonomous parts processing. The company is targeting 50,000 to 100,000 units in 2026, with the Fremont line designed to reach one million annually. The manufacturing focus directly addresses the cost gap: China's humanoid bill of materials currently runs roughly $50,000 versus $130,000 in the US. Closing that gap requires exactly the kind of scale that Tesla's automotive DNA was built to deliver.

The IP Undercurrent

Patent data adds another dimension. WIPO reported 3.7 million global patent filings in 2024, up 4.9% year-over-year. China accounted for 1.8 million, three times the US total, and leads in computer technology patents at 15.2% of filings. The US leads in digital communication at 8.7%, Japan in electrical machinery, Germany in transport.

Quantity is not quality. The Western advantage in foundational robotics IP, actuator design, sensing systems, motion-planning algorithms, remains significant. But China's patent velocity, combined with its deployment scale, creates a compounding feedback loop: more robots in the field means more real-world training data, which feeds better AI models and faster iteration.

What This Means

The robotics race is a technology and infrastructure race, and infrastructure races produce durable winners. The country that deploys at the greatest scale accumulates the manufacturing capacity, training data, supply chain expertise, and cost advantages that compound over decades.

China treats robotics deployment the way the US once treated interstate highways and semiconductor fabs: as strategic infrastructure that enables everything else. The US approach remains largely market-driven, dependent on private capital and individual corporate bets like Tesla's Optimus pivot or Amazon's acquisition spree. American capital markets can move faster on breakthroughs, Figure AI's $39 billion valuation is proof of that ecosystem's power. But market-driven deployment without coordinated industrial policy risks leaving the US permanently behind on the installation curve that determines long-term competitiveness.

For investors, the signal is clear. Robotics M&A deal values have grown sevenfold in a decade. Inflows are concentrated in industrial machinery ($69.6 billion) and data processing services ($61.1 billion), the physical and digital layers of the automation stack. The companies that will define the next decade sit at the intersection of robotics hardware, AI software, and scalable manufacturing. The next two to three years will be decisive in determining whether enough of them are American.

Source Attribution

Sources: International Federation of Robotics (IFR) World Robotics 2025; WIPO World Intellectual Property Indicators 2025; FactSet Transaction and Private Markets data; Fortune Business Insights; Bloomberg; CNBC; company disclosures.